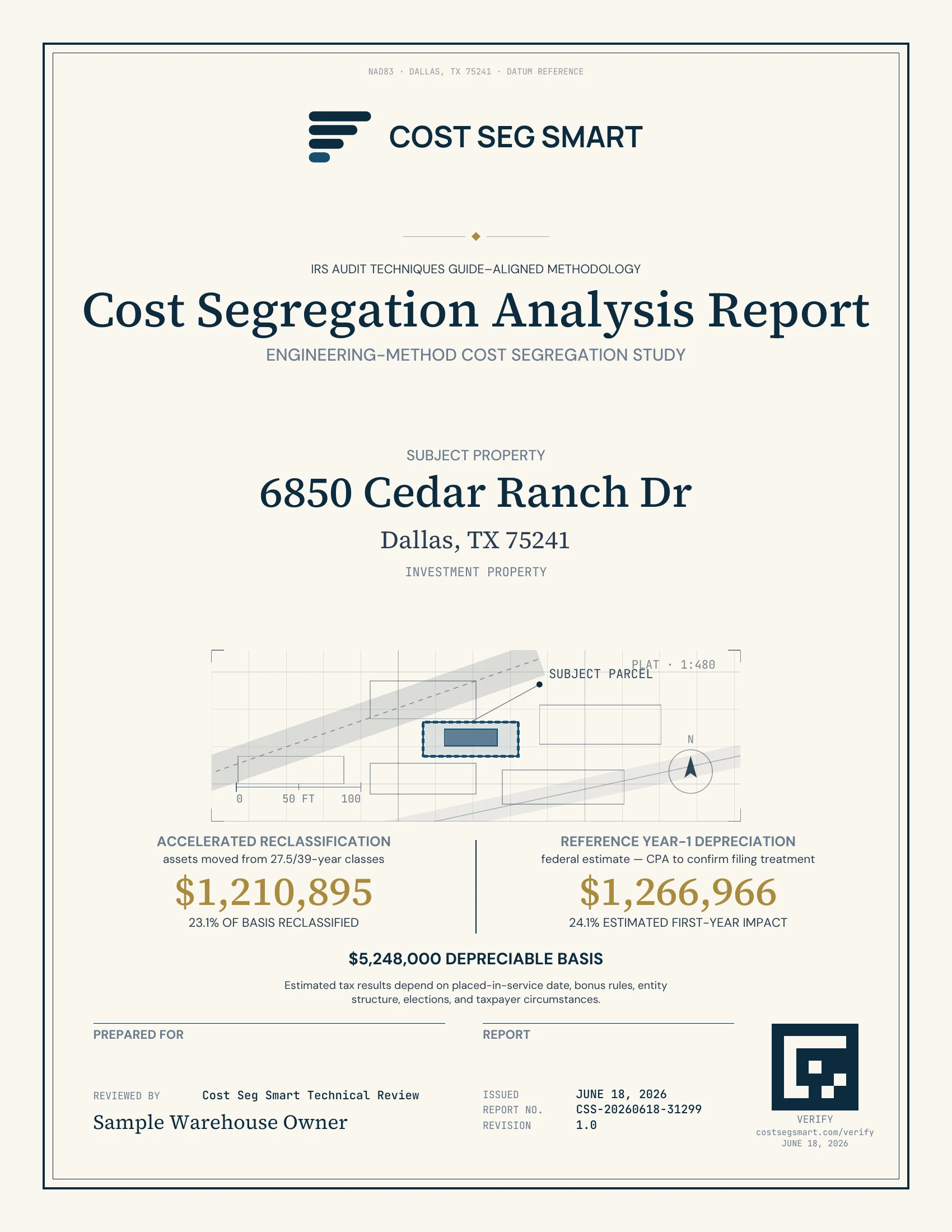

Sample warehouse cost segregation report

A real, redacted Cost Seg Smart warehouse / distribution property study, shown so you can see exactly what the deliverable contains and how the component allocation works. The numbers below come from one illustrative Iowa City, IA example.

Warehouse cost segregation reclassifies depreciable basis from the 39-year shell into 5-, 7-, and 15-year MACRS classes, which 100% bonus depreciation makes deductible in Year 1. There is no single expected percentage. In this one illustrative Iowa City, IA sample on $24,136,800 of basis, $4,016,250 (16.6% of basis) was reclassified into accelerated classes, for an illustrative Year-1 deduction of about $4,295,702. Your result depends on property age, finishes, equipment, and land value.

This Iowa City, IA study, by the numbers

One illustrative sample, not a benchmarkIllustrative result from one sample report. Actual reclassification varies substantially with property age, improvements, tenant finish, equipment, land value, and other facts. Not a benchmark or expected range. Request the full sample PDF →

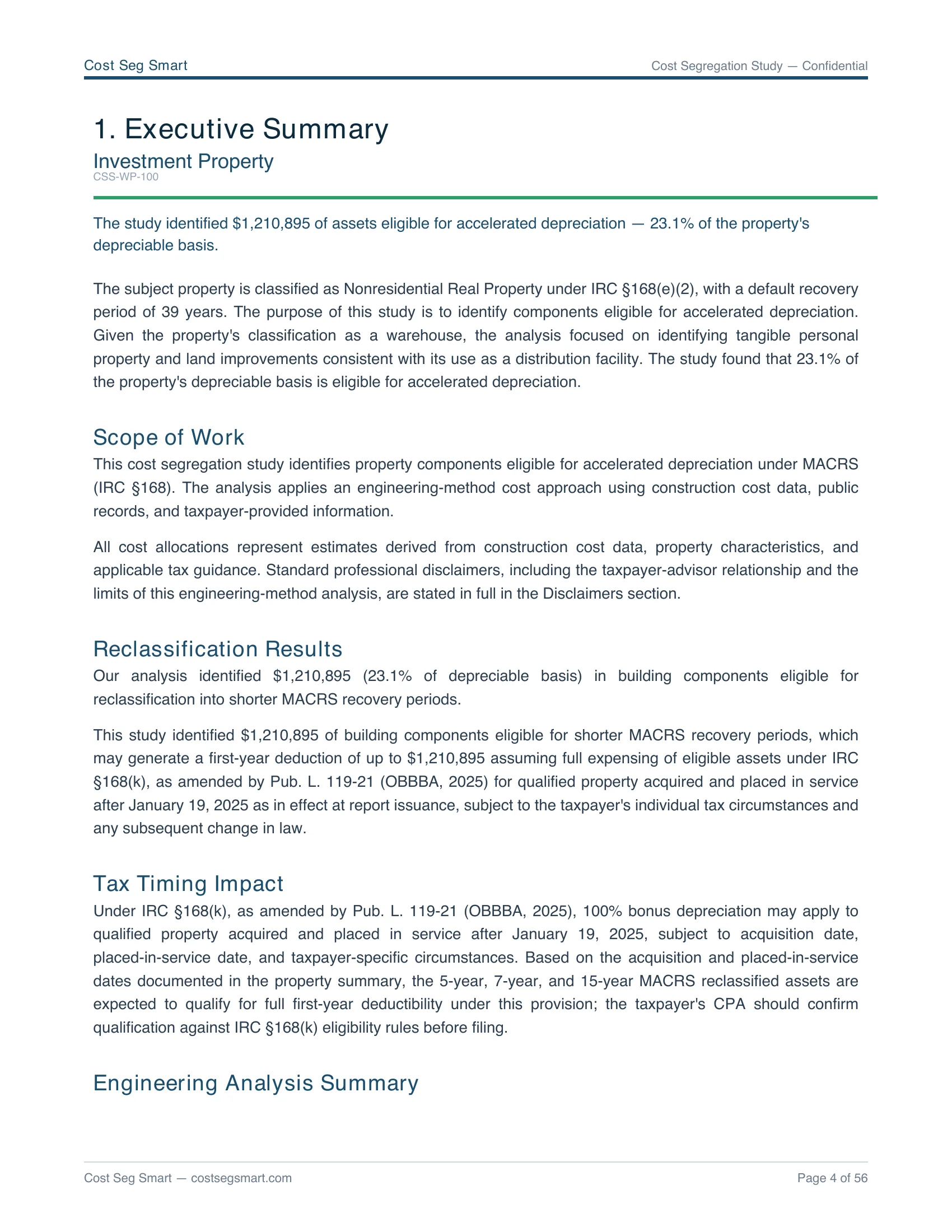

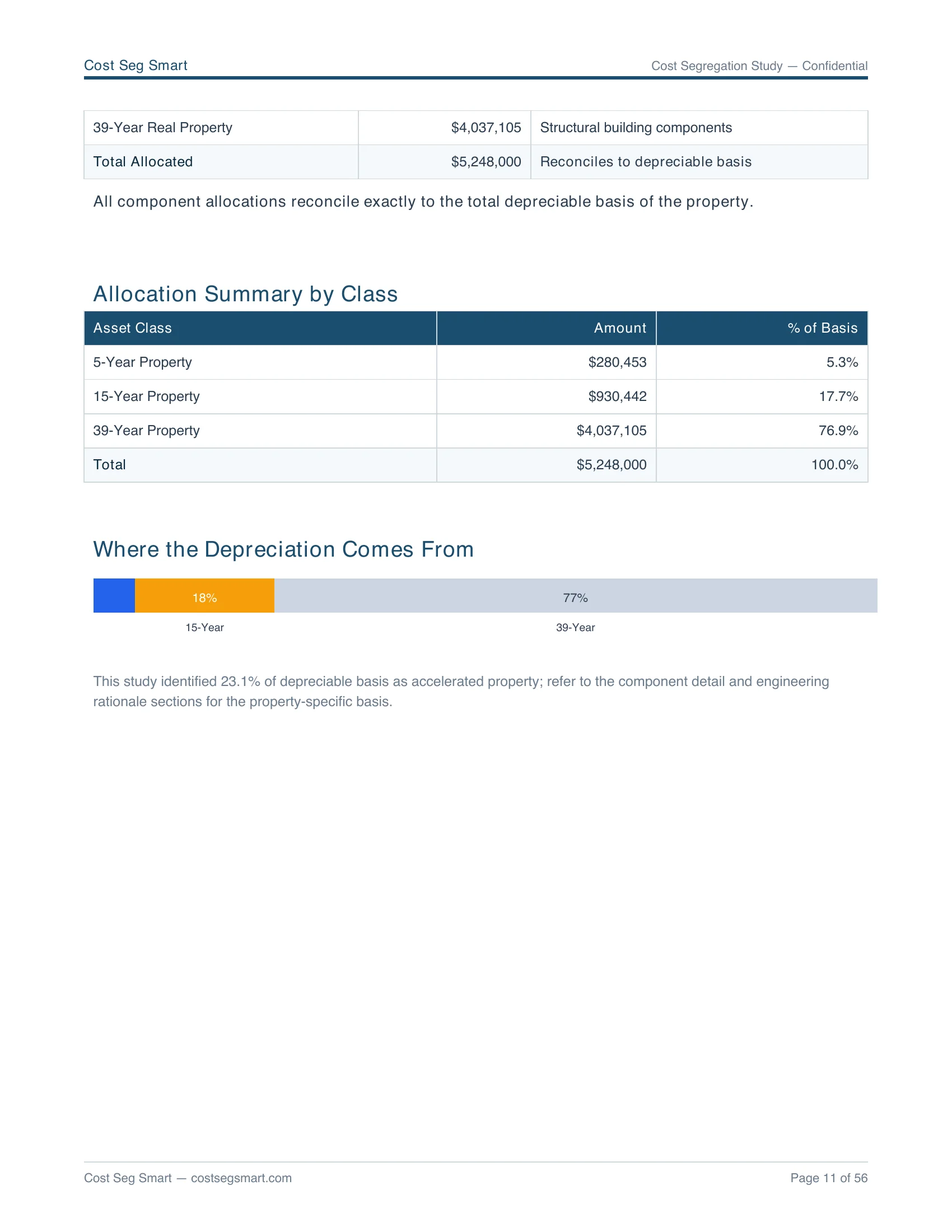

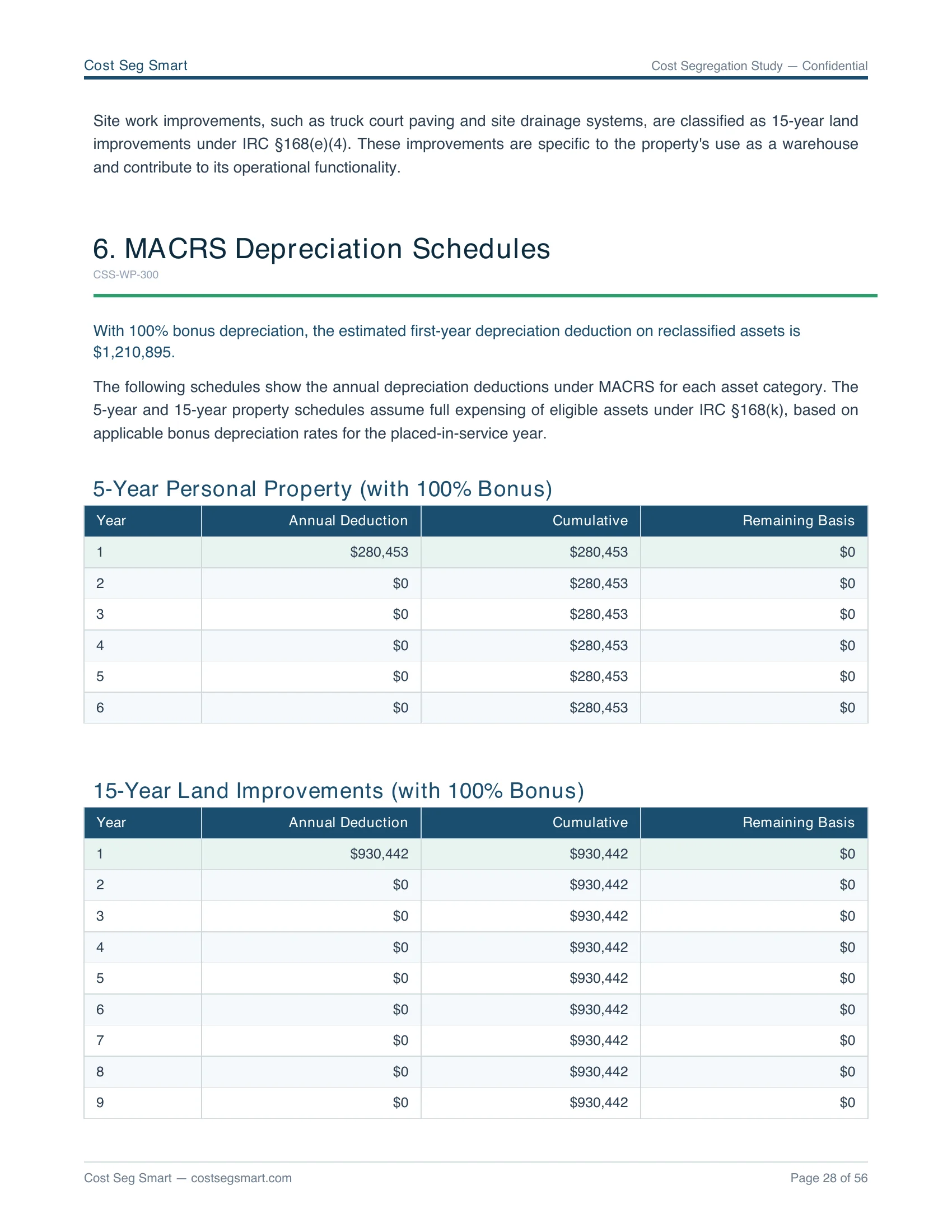

Inside the report: actual pages

Real pages from a warehouse study (an illustrative Iowa City, IA subject property, figures redacted where needed). This is the actual deliverable, not a brochure mockup. Click any page to open it full size.

The report itself

Engineering analysis summary

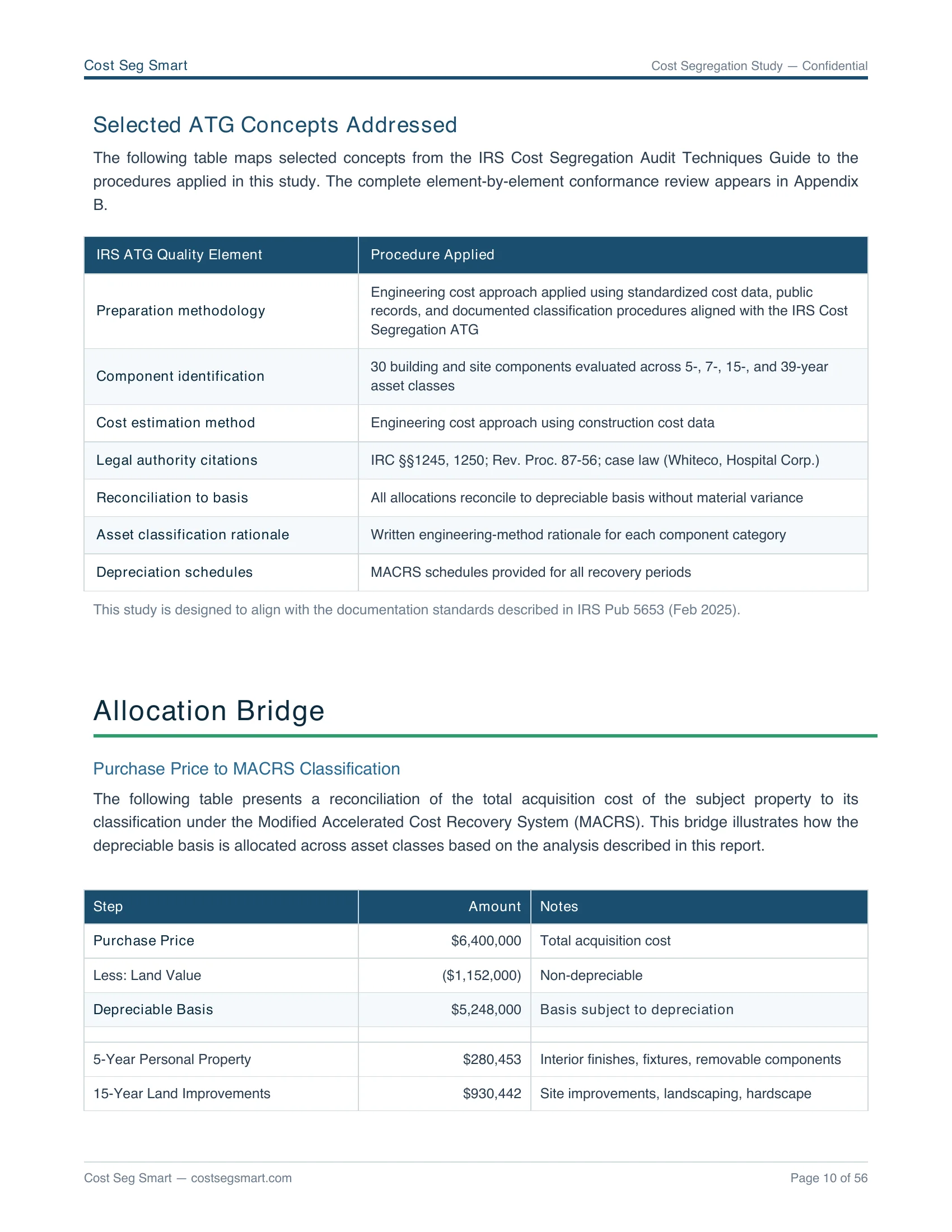

Allocation by asset class

MACRS depreciation schedules

IRS methodology, addressed

Illustrative result from one sample report. Actual reclassification varies substantially with property age, improvements, tenant finish, equipment, land value, and other facts. Not a benchmark or expected range.

Why warehouses lean on 15-year site work

This illustrative Dallas distribution warehouse reached 23.1%, and most of it came from the yard, not the building. Distribution facilities frequently contain:

- ✓ Truck courts and heavy-duty paving

- ✓ Yard and dock lighting

- ✓ Perimeter fencing and security gates

- ✓ Dock levelers and dock equipment

- ✓ Specialty electrical serving equipment

- ✓ An office build-out within the warehouse

Warehouses are shell-heavy buildings, so the 15-year site-work bucket usually drives the result more than 5-year personal property. A warehouse on a small lot with little paving reclassifies less.

Illustrative component allocation

Distribution warehouses are driven by a large 15-year site-work bucket (truck courts, paving, yard lighting) more than 5-year personal property. Below is how this one sample report split its $24,136,800 depreciable basis across MACRS classes (Section 3 of the deliverable lists every component line by line).

| MACRS class | Allocated basis | % of basis |

|---|---|---|

| 5-Year Personal Property Dock equipment, specialty electrical, fixtures | $1,585,602 | 6.6% |

| 15-Year Land Improvements Truck courts, paving, yard lighting, fencing | $2,430,648 | 10.1% |

| 39-Year Commercial Shell Structural building, envelope, base systems | $20,120,550 | 83.4% |

| Accelerated (5/7/15-year) | $4,016,250 | 16.6% |

Where the depreciation comes from

Illustrative result from one sample report. Actual reclassification varies substantially with property age, improvements, tenant finish, equipment, land value, and other facts. Not a benchmark or expected range. Tax-side figures assume the placed-in-service year's §168(k) bonus rate and an assumed entity rate; actual depends on entity structure, state conformity, passive-activity limits (§469), and at-risk basis (§465). Verify with your CPA before filing.

Why your result will differ from this example

No two warehouse properties reclassify the same. The 16.6% above came from one specific building. Yours depends on:

- → Property age — newer buildings carry more reclassifiable finishes and systems.

- → Renovations and tenant improvements — recent build-outs add 5- and 7-year assets.

- → Equipment intensity — equipment-heavy uses (kitchens, service bays, medical) reclassify more.

- → Site work — extensive paving, parking, and landscaping drive the 15-year bucket.

- → Land value — a higher land share leaves less depreciable basis to reclassify.

- → Local construction costs and finish level — these shift each component's allocated basis.

That is why we model your specific property before you commit, and never apply a rule-of-thumb percentage. The IRS Cost Segregation Audit Techniques Guide (Pub 5653) warns against template and rule-of-thumb studies for exactly this reason.

Why CPAs file straight from these reports

Every warehouse study delivers the same six-section structure, so your CPA can file without rework. Depth scales with property size and lookback complexity.

Executive summary

The one-page summary your CPA reads first: total reclassified, the Year-1 deduction, and the technical-review sign-off.

Engineering methodology

Shows why each asset was assigned its depreciation class, and documents the reasoning behind every allocation.

Component allocation tables

Every component (typically 40 to 80 line items) mapped to its asset class and MACRS life, with subtotals that reconcile to the depreciable basis.

Depreciation schedules

Year-by-year MACRS deduction tables, formatted to drop straight onto Form 4562, with bonus depreciation flagged for the placed-in-service year.

Section 481(a) lookback workpaper

For a Form 3115 catch-up: the cumulative Section 481(a) adjustment and a line-by-line reference for your tax preparer (when applicable).

Documentation and audit support

A cost-source citation for every component, the classification rationale, and the methodology narrative an examiner asks for. Support for the life of the study.

How the report addresses IRS examiner standards

The IRS Cost Segregation Audit Techniques Guide (Pub 5653) lists the elements an examiner reviews, and the report maps to each one: the engineering methodology and component allocation document every classification, each component carries a Rev. Proc. 87-56 asset-class citation with its rationale, and Appendix B walks all 13 elements of Pub 5653 Chapter 4 one at a time, naming the report section that satisfies each. Appendices C and D carry the Rev. Proc. 87-56 / IRC framework and the supporting case law and IRS rulings; Appendix E covers workpaper retention and the records to keep alongside the report.

Every study includes audit documentation, and written answers to your CPA's technical questions for the life of the study, at no additional charge. Full scope at /audit-defense/.

How this compares with traditional firms

Traditional-firm figures are typical industry ranges; confirm pricing and scope directly with any vendor. For the full firm-by-firm breakdown see best cost segregation companies.

Report questions

Is this a real warehouse cost segregation report?

What reclassification percentage should I expect for a warehouse?

Can I download the sample PDF?

Does the report include Form 3115 for a lookback?

How is this different from a benchmark or a percentage range?

See your warehouse's real numbers, not a sample's.

We model your specific property before you pay. Order an engineered study or request the full illustrative warehouse sample PDF first.

Estimate your warehouse savings · All report examples · Industrial cost segregation · Form 3115 walkthrough · Audit defense