Commercial cost segregation services — by asset class.

Engineering-based reclassification studies for office, retail, restaurant, industrial, medical office, and mixed-use property — built on the IRS framework engineering firms use, with written audit-support scope and asset-class-specific methodology.

Reviewed by Cost Seg Smart Editorial Team · First published: · Last reviewed: · Sources

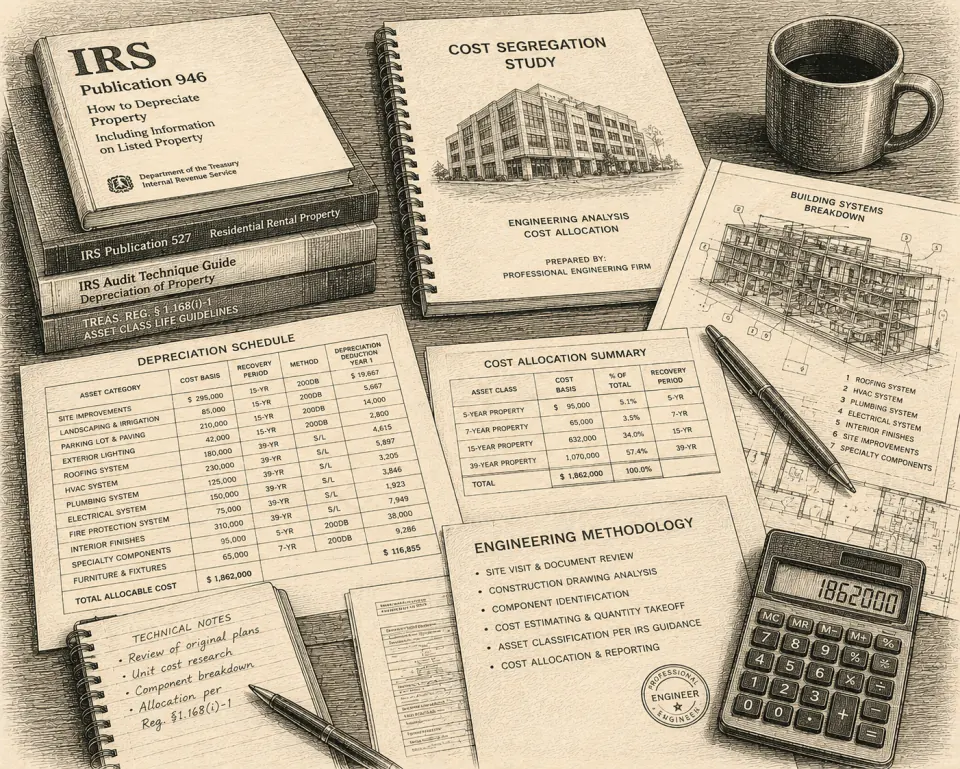

Commercial cost segregation is the engineering-based reclassification of a commercial property's depreciable basis from the default 39-year MACRS schedule into 5-, 7-, and 15-year property classes per Rev. Proc. 87-56.

| Asset class | Median reclassification | Typical Year-1 tax savings (top bracket) | Study cost (from) |

|---|---|---|---|

| Office | 29.1% | $95K–$220K on $1.5M–$3M | $995 |

| Retail | 32.0% | $110K–$240K on $1.5M–$3M | $995 |

| Restaurant | 30.5% | $100K–$230K on $1.5M–$3M | $995 |

| Industrial / warehouse | 20.3% | $70K–$150K on $1.5M–$3M | $995 |

| Medical office | 33.5% | $115K–$250K on $1.5M–$3M | $995 |

| Mixed-use | 25.7% | $85K–$190K on $1.5M–$3M | $995 |

Six commercial asset classes, six engine paths.

A $2M restaurant doesn't reclassify like a $2M office condo. Different components, different IRS class lives, different math. We differentiate by asset class and by subtype within each class. Reclassification ranges below are medians from the 2026 benchmarks dataset (n=412); your study's number depends on basis allocation, finish density, and use type.

How basis is reclassified across recovery periods.

Every commercial study reclassifies basis from the default 39-year structural shell into shorter MACRS classes per Rev. Proc. 87-56. The diagram below shows median splits across asset classes from the 2026 benchmarks dataset. 5-year is FF&E + decorative finishes; 15-year is land improvements + Qualified Improvement Property; 39-year is the building shell that doesn't reclassify.

Note. Right column shows total reclassified basis (5-yr + 15-yr); residual is 39-year shell. 7-year property (where applicable) folded into 5-year for legibility. 27.5-year residential class shown only on mixed-use (residential floors). Source: Cost Seg Smart 2026 Benchmarks Report (n=412), CC-BY 4.0.

What the 2026 benchmarks data shows.

Original dataset: 260 cost-seg studies analyzed across 13 property types. Methodology and full IQR distributions at /research/benchmarks-2026/. Below: median reclassification % by commercial asset class.

Nine commercial properties, nine outcomes.

Year-1 federal tax savings shown at top federal bracket, assuming 100% bonus depreciation on the reclassified portion. Your study's number will vary with basis allocation, finish density, and your CPA's review.

What makes commercial different from residential.

Commercial property doesn't follow the same classification path as a single-family rental. Five subtype-aware mechanisms differentiate the analysis — each grounded in the published IRS class-life and finish-density guidance, applied per property.

Office intensity tiers (economy / standard / premium / luxury)

Office reclassification depends heavily on tenant fit-out density. The engine separates economy (Class C suburban, basic finishes), standard (Class B with moderate tenant build-out), premium (Class A with executive suite finishes), and luxury (high-end law-firm or finance interiors). Each tier has its own component mix multipliers — premium finishes drive 5- and 7-year property up; economy keeps the building shell closer to the 39-year baseline. Result: a $2M Class A office surfaces ~32% reclassification while a $2M Class C economy office surfaces ~24%.

Restaurant subtype scaling (QSR / full-service / brewery)

Restaurants top out near 40% reclassification because of FF&E density. The engine scales by subtype: quick-service restaurants have moderate kitchen equipment and standard finishes; full-service restaurants have full commercial kitchens, exhaust hood systems, and decorative front-of-house finishes; breweries add specialty MEP, fermentation equipment, and walk-in cold storage. A $1.6M brewery reclassifies more aggressively than a $1.6M fast-casual — the subtype scaling captures it without manual override.

Industrial finish-score classifier

Industrial owners see the widest reclassification range in our dataset: 19.5% to 29.8% IQR. A finish-score classifier separates pure warehouse (low FF&E, low MEP, basic finishes; 16–20% reclass) from flex bay (warehouse plus finished office combo; 24–28%) from industrial-office (close to commercial office economics; 28–32%) from light industrial and manufacturing (specialty MEP, process equipment; 24–32%). Mezzanines, dock equipment, and yard improvements get evaluated per case for 5- vs 15-year vs 39-year treatment.

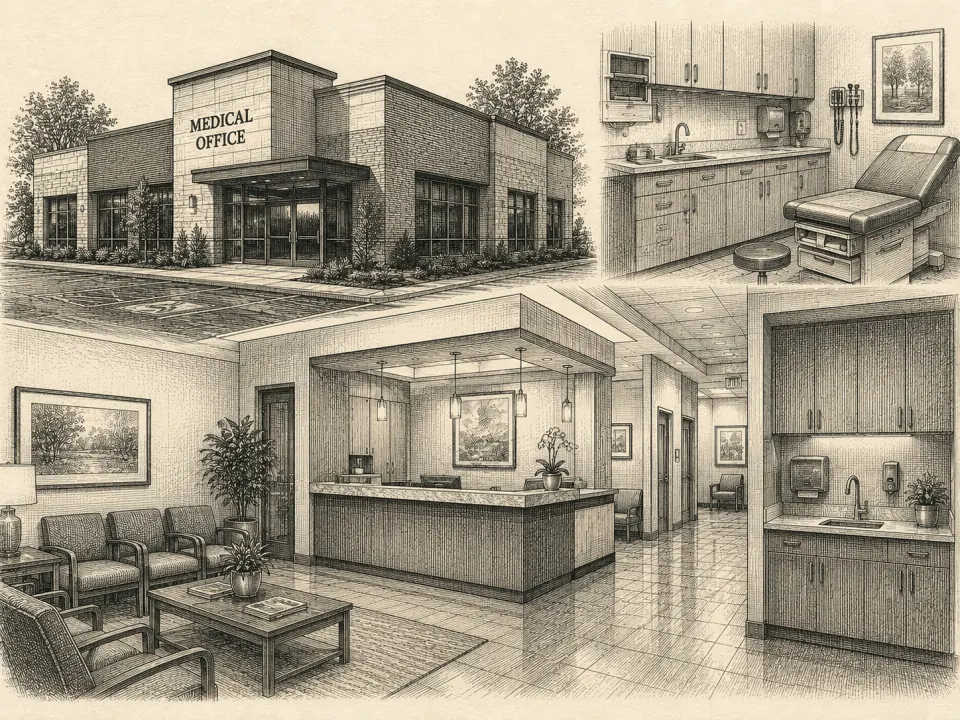

Medical office multipliers (specialty plumbing + casework)

Medical office owners see the highest reclassification ratio in our dataset: 33.5% median, best-in-class. We apply medical-office-specific multipliers for specialty plumbing (medical gas, hand-wash stations, vacuum lines), specialty fixtures (exam-room casework, dental chairs, ambulatory surgery built-ins), specialty MEP, and decorative tenant-fit interiors. Multi-physician primary care, dental practices, and ambulatory surgery centers consistently surface 30%+ reclassification.

Mixed-use blending (residential + commercial mix)

Mixed-use blends commercial and residential component economics. The engine handles the allocation per square footage: ground-floor retail follows commercial reclassification (32% median); upper-floor residential follows residential (16–22%); shared building shell allocated proportionally. The result is a weighted reclassification specific to the property's mix — a 4,000 sf retail / 12,000 sf residential mixed-use will surface different ratios from a 8,000 sf retail / 8,000 sf residential mix at the same total basis.

Commercial study pricing.

Pricing scales by basis band and property type. Standard Commercial, Multifamily 5+, and Industrial / Warehouse each have their own band ladder; Specialty Commercial (medical, restaurant, hospitality, manufacturing) is scoped per engagement. Built on the same MACRS classification framework and IRS Pub. 5653 documentation standards engineering firms use — the price difference reflects an efficient delivery model, not lower rigor.

What we provide if your study is examined.

Audit-support scope is committed in writing — same posture as engineering firms charging $5,000–$15,000. We provide engineering documentation; your CPA, EA, or attorney provides taxpayer representation under Circular 230. The summary below is excerpted; full scope and 13-element ATG framework at /audit-defense/.

See the deliverable for your asset class.

Six commercial sample PDFs available — same structure for every study. Methodology section, full component schedule with RSMeans line citations, year-by-year depreciation tables, land valuation methodology, MACRS classification with Rev. Proc. 87-56 anchor, engineer attestation, and Form 3115 readiness pack for lookback applicability.

When to skip this and use a traditional firm.

Not every commercial property fits a systematized engineering workflow. Below are four patterns where the right answer is to engage a traditional engineering firm with an on-site visit, even at $5,000–$15,000.

- $15M+ properties — basis large enough that even small reclassification differences justify on-site engineering and a custom scoping engagement. We'll quote on request.

- Ground-up development — cost segregation applies after a property is placed in service. During construction, basis is capitalized under §263A. Talk to your CPA about §263A capitalization first; cost-seg comes later.

- Multi-parcel campus deals — three or more parcels under a single acquisition with shared improvements requires custom basis allocation. Our automation isn't built for split-parcel basis. Refer to a traditional firm.

- Selling within 12 months without a §1031 exchange — recapture under §1245 + §1250 eats most of the benefit when held under 24 months. Pair with a §1031 to defer the recapture, or skip cost-seg and use straight-line.

Commercial cost-seg questions.

Does cost segregation work on a $1M+ commercial property?

How does cost seg differ for office vs. restaurant vs. industrial?

What's QIP and how is it treated?

Can I use cost seg on a property held in an LLC or S-corp?

Is cost seg compatible with §1031 exchanges?

What's partial disposition and when does it apply?

How is tenant improvement (TI) basis handled?

How does Cost Seg Smart handle warehouses with mezzanines or industrial flex?

What's the lookback option for properties already in service?

What if the IRS audits my commercial cost-seg study?

Sources & primary references.

- IRS Cost Segregation Audit Techniques Guide (Pub. 5653) — methodology framework for every defensible study.

- Rev. Proc. 87-56 — Asset Class Lives — IRS recovery period assignments per asset class.

- 26 U.S.C. §168 — MACRS — statutory basis for cost-seg reclassification + §168(k) bonus depreciation.

- 26 U.S.C. §481(a) — method-change adjustment statute permitting Form 3115 lookback.

- Hospital Corp. of America v. Commissioner, 109 T.C. 21 (1997) — Tax Court decision establishing engineering-based reclassification framework.

- AmeriSouth XXXII v. Commissioner, T.C. Memo. 2012-67 — documentation standards examiners apply today.

- Rev. Proc. 2015-13 — automatic-consent for depreciation method changes (DCN 7).

- Cost Seg Smart 2026 Benchmarks Report (n=412) — original dataset; source for reclassification % ranges quoted on this page.

The next step depends on where you are in the evaluation. Most commercial owners start with the intake form for a property-specific written quote.

No checkout. Reclassification estimate, Form 3115 eligibility, sample report — within one business day.

Or skip ahead: run an instant estimate · order directly