Most residential rental properties depreciate over 27.5 years — about $11,000 per year on a $400K property. But with cost segregation, investors routinely deduct $45,000 to $100,000 in the first year instead.

Same property. Same IRS rules. Different timing. Here's exactly how it works.

Rental property depreciation lets you write off the cost of a residential rental building over 27.5 years — roughly $11,600/year on a $400K property after subtracting land. Many investors accelerate 20–35% of that basis into Year 1 with cost segregation, but whether that makes sense depends on property value, tax bracket, and hold period. See a sample cost segregation report for how this looks in practice.

Key Takeaways

- Residential rentals depreciate over 27.5 years; commercial property uses 39 years

- Only the building depreciates — land (typically 15–25% of purchase price) does not

- Cost segregation reclassifies 20–35% of building components into 5, 7, and 15-year schedules

- Bonus depreciation is currently 100% as of 2025 under the One Big Beautiful Bill Act

- Recapture applies when you sell — you're changing timing, not avoiding tax

What Is Rental Property Depreciation?

The IRS considers your rental building a wasting asset — it wears out over time. They let you deduct that wear as a tax expense, spread over what they call a "recovery period." For residential rental property, that period is 27.5 years. For commercial buildings, it's 39 years.

Only the building depreciates. Land doesn't wear out, so the IRS won't let you deduct it. On a typical purchase, 15–25% of the price is allocated to land (varies by location — Manhattan is mostly land, rural Oklahoma is mostly building).

Here's what that looks like on a $400K rental:

Basic depreciation — $400K single-family rental

That $11,636 comes off your taxable rental income every year for 27.5 years. It's a real deduction — it reduces your tax bill whether or not you spent a dime on the property that year. And it's available to every rental property owner automatically.

That's the default. But many investors don't actually wait 27.5 years.

The Real Comparison

Here's the number that changes everything:

| Scenario | Year 1 Deduction |

|---|---|

| Standard 27.5-year straight-line | $11,636 |

| With cost segregation + 100% bonus depreciation | $45,000 – $90,000 |

Same property. Same IRS rules. The difference is which depreciation schedule the building components are assigned to — and whether you front-load the deductions into Year 1 or spread them over nearly three decades.

How Depreciation Actually Works

Straight-line depreciation (the default)

When you buy a rental and don't do anything special, your CPA puts the entire building on a 27.5-year straight-line schedule. Every year, you deduct the same amount: basis ÷ 27.5. It's simple, predictable, and leaves a lot of deductions on the table for later years.

Accelerated depreciation (what changes)

Not everything in a building has a 27.5-year life. The appliances in the kitchen? Five years. The carpet on the floors? Five years. The landscaping out front? Fifteen years. These aren't arbitrary — these are the IRS's own MACRS property class assignments under Revenue Procedure 87-56.

The problem is that most CPAs default to lumping everything into the 27.5-year building. It's simpler. It's conservative. And it costs investors thousands of dollars a year in missed front-loaded deductions.

Where cost segregation fits

This is where cost segregation becomes relevant. A cost segregation study is an engineering-based analysis that identifies which components of your property qualify for shorter depreciation schedules. It doesn't create new deductions — it reclassifies components that were always eligible for faster depreciation but were never broken out separately.

how the classification process works →

What Can Be Depreciated Faster

| Category | Recovery Period | Examples |

|---|---|---|

| 5-year property | 5 years | Appliances, carpet, decorative lighting, some cabinetry, window treatments |

| 7-year property | 7 years | Office furniture, specialized equipment, certain kitchen equipment |

| 15-year property | 15 years | Landscaping, driveways, fencing, pools, parking areas, outdoor lighting |

| Structural (building shell) | 27.5 years | Walls, roof, foundation, framing, plumbing, electrical (structural) |

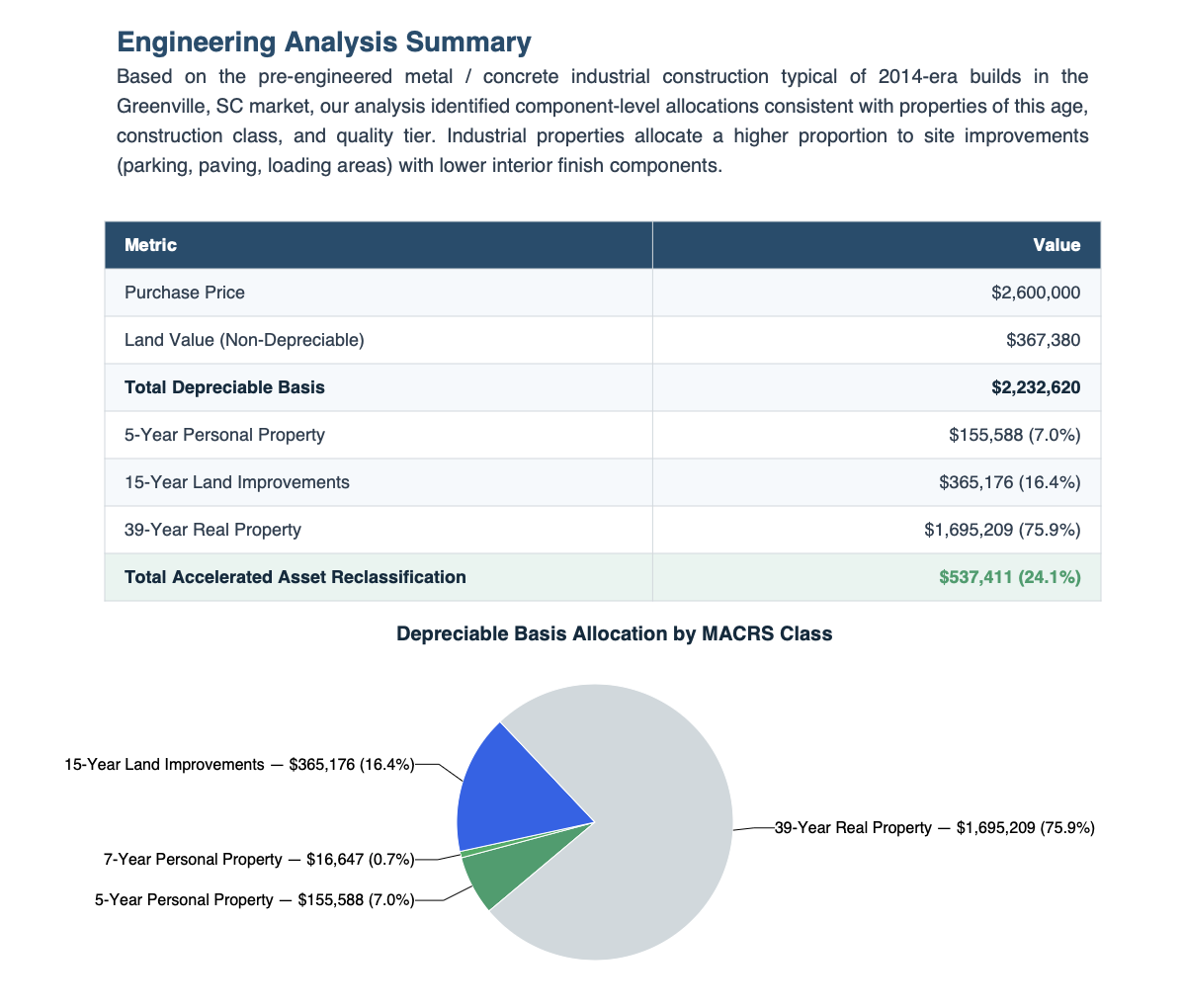

For a typical unfurnished single-family rental, roughly 18–25% of the depreciable basis falls into the 5-year and 15-year categories. For a furnished short-term rental with beds, couches, TVs, and kitchen equipment, that number jumps to 28–35% because all the furniture and décor qualifies as 5-year personal property.

Bonus Depreciation

Bonus depreciation under IRC §168(k) is an additional first-year deduction that applies to MACRS property with a recovery period of 20 years or less. That's exactly the 5, 7, and 15-year classes that cost segregation reclassifies components into.

As of 2025, bonus depreciation is 100% under the One Big Beautiful Bill Act. The timeline has moved around:

| Year | Bonus Rate |

|---|---|

| 2017 – 2022 | 100% |

| 2023 | 80% |

| 2024 | 60% |

| 2025+ | 100% (restored under OBBBA) |

At 100% bonus, every dollar reclassified by cost segregation can be deducted in Year 1. That's what makes the $11K vs $45K+ comparison possible — you're taking 5–15 years of future depreciation and compressing it into the current tax year.

Depreciation Recapture: The Honest Part

This is where most guides either skip the details or try to scare you. Neither is helpful.

When you sell a rental property, the IRS requires you to "recapture" the depreciation you've taken. For real property (the 27.5-year building), recapture is taxed at up to 25% under IRC §1250. For personal property (the 5-year and 7-year assets identified by cost segregation), recapture is taxed at ordinary income rates under IRC §1245.

You're not avoiding tax. You're changing when you pay it.

And the time value of that change matters. If cost segregation saves you $50,000 in Year 1 and you invest that savings at 8% for 7 years, it grows to roughly $85,000. When you sell and pay recapture on the accelerated portion, you're paying back with dollars that are worth less than the dollars you saved. The math gets even better if you hold longer, or if you do a 1031 exchange, which defers recapture entirely.

For the full breakdown of how depreciation recapture works after cost segregation, we go deeper elsewhere.

Where Cost Segregation Fits

You don't need cost segregation to depreciate your rental property. The 27.5-year deduction is automatic. But if you want $45,000 in Year 1 instead of $11,000, cost segregation is how you get there.

A cost segregation study is an engineering-based analysis that breaks your property into its individual components — foundation, framing, roofing, flooring, appliances, landscaping, fixtures — and assigns each one to its proper MACRS depreciation class. The study produces a 40+ page report with component-level classifications, depreciation schedules, and the documentation your CPA needs to file the accelerated depreciation on your return.

Typical results:

| Property Type | Typical Reclassification | Year 1 Tax Savings (32% bracket, $500K property) |

|---|---|---|

| Unfurnished SFR | 18–25% | $23,000 – $32,000 |

| Furnished STR (Airbnb) | 28–35% | $36,000 – $45,000 |

| Duplex / Triplex | 20–28% | $26,000 – $36,000 |

Studies start at $495 for properties under $300K ($795 for $300K–$1M). A look at recent pricing across providers is available on CostSegregationReviews.com.

For STR owners who materially participate, these losses aren't just passive rental deductions — they can offset W-2 and active income under the short-term rental exception to IRC §469.

Should You Actually Do This?

Quick qualification check

- Property value above $100K

- Federal tax bracket 24% or higher

- Planning to hold the property for 3+ years

- Comfortable with slightly more complex depreciation schedules on your return

- If STR: willing to document 100+ hours of participation per year

If you checked all five, the math almost certainly works. If you checked 3–4, run the numbers first. If you checked 2 or fewer, standard depreciation may be sufficient for now.

Full Worked Example

$500K unfurnished rental — standard vs. cost segregation

That's a $21,500 difference in Year 1 tax savings. On the same property. With the same IRS rules. The only variable is whether the building components were identified and classified properly.

Related Reading

Frequently Asked Questions

Yes. You can start depreciating a rental property at any time after it's placed in service. If you've been using standard straight-line depreciation and want to switch to accelerated depreciation via cost segregation, you file Form 3115 (Change in Accounting Method) with your next tax return. The Section 481(a) adjustment lets you catch up all the missed accelerated depreciation in a single year — no need to amend prior returns.

For unfurnished single-family rentals, typically 18–25% of the depreciable basis gets reclassified into shorter MACRS schedules. For furnished short-term rentals with significant FF&E (furniture, fixtures, equipment), the reclassification rate is typically 28–35%. See our cost segregation benchmarks for typical percentages by property type.

No. Every rental property owner can claim standard straight-line depreciation over 27.5 years without a cost segregation study. Cost segregation is optional — it accelerates the depreciation by reclassifying building components into shorter recovery periods. The study is what identifies which components qualify and provides the engineering documentation to support the reclassification.

When you sell, the IRS requires you to "recapture" the depreciation you've taken. Real property depreciation is recaptured at up to 25% under IRC §1250. Personal property is recaptured at ordinary rates under IRC §1245. However, the time value of accelerated deductions usually wins — and a 1031 exchange defers recapture entirely. See our depreciation recapture deep dive for full details.

Effectively yes. The IRS requires you to reduce your cost basis by the "allowable" depreciation — the depreciation you were entitled to take, whether or not you actually claimed it. If you skip depreciation and later sell, the IRS calculates your gain as if you had taken it. There is no benefit to skipping depreciation on a rental property.

Yes, but the depreciable basis is the lesser of your adjusted cost basis or the fair market value on the date of conversion. If your home appreciated significantly, you can only depreciate the lower of the two values. Cost segregation can be applied to converted properties, and a lookback study with Form 3115 can capture missed depreciation from prior years. See our full guide on primary residence to rental conversions.

27.5 years is for "residential rental property" (80%+ of gross rental income from dwelling units). 39 years is for nonresidential commercial buildings. Short-term rentals typically use 27.5 years because they're dwelling units, even though the operation resembles a commercial business. Mixed-use properties split between the two based on square footage or rental income allocation.

Bonus depreciation under IRC §168(k) allows you to deduct 100% of the cost of qualifying property in the year it's placed in service. It applies to assets with a MACRS recovery period of 20 years or less — the 5, 7, and 15-year classes that cost segregation reclassifies components into. As of 2025, bonus depreciation is 100% under the One Big Beautiful Bill Act. The building itself (27.5 or 39-year property) does not qualify for bonus — only the reclassified components do.

Related Articles

MACRS Depreciation Explained

The 5, 7, 15, 27.5, and 39-year property classes and how cost segregation reclassifies between them.

Depreciation Recapture After Cost Segregation

What happens when you sell, how recapture is calculated, and why the math usually still works.

What $495 Actually Gets You

Same RSMeans data, same IRS rules, same 35-page report. Three real examples with tax math.