MACRS Depreciation Explained

MACRS is the depreciation system every rental property uses: 5, 7, 15, 27.5, and 39-year classes. How cost segregation reshuffles them for bigger Year-1 losses.

MACRS is the depreciation system every rental property uses: 5, 7, 15, 27.5, and 39-year classes. How cost segregation reshuffles them for bigger Year-1 losses.

MACRS (Modified Accelerated Cost Recovery System) is the IRS-mandated depreciation method for virtually all business and investment property placed in service after 1986. It assigns building components to recovery periods of 5, 7, 15, 27.5, or 39 years. Cost segregation reclassifies components into the shorter classes, dramatically front-loading depreciation deductions.

Key Takeaways

- MACRS (Modified Accelerated Cost Recovery System) is the depreciation system nearly every rental and commercial property has used since 1986

- There are five main property classes: 5-year, 7-year, 15-year, 27.5-year (residential), and 39-year (commercial) — each with different recovery math

- Cost segregation reclassifies components of a building into shorter MACRS classes, front-loading deductions dramatically

- With 100% bonus depreciation permanently restored in 2025 under the OBBBA, components in the 5, 7, and 15 year classes can be fully deducted in Year 1

What Is MACRS and Why Almost Every Property Uses It

If you own an investment property in the United States, you’re almost certainly depreciating it under MACRS, whether you know it or not. MACRS stands for Modified Accelerated Cost Recovery System, and it’s been the standard for U.S. depreciation since the Tax Reform Act of 1986. Before MACRS, there was ACRS (same idea, slightly different math). Before ACRS, there was ADR (depreciation by useful life). The whole history is Congress trying to simplify something that never really simplifies.

Here’s the one-sentence explanation of MACRS: every depreciable asset gets assigned to a property class, and each property class has a recovery period and a depreciation method. You take the property’s basis, apply the schedule, and that tells you your deduction for each year.

For a rental property bought at $500K with $100K allocated to land, your depreciable basis is $400K. Under default MACRS rules for residential rental, that $400K spreads over 27.5 years at roughly $14,545 per year. That’s it. That’s the default.

The default MACRS schedule is where most property owners stop. What they miss is that MACRS also allows faster recovery for components of the building — appliances, flooring, cabinets, HVAC subsystems, landscaping, driveways, site improvements. Cost segregation is the engineering process of separating those components out and giving them their proper MACRS classification instead of bundling them into the 27.5 or 39 year building basis.

The MACRS Property Classes

Here are the classes most relevant to real estate investors, in order of recovery period:

| Class | Recovery Period | Method | Examples of Components |

|---|---|---|---|

| 5-year property | 5 years | 200% declining balance | Appliances, carpeting, furniture, fixtures, decorative lighting |

| 7-year property | 7 years | 200% declining balance | Office furniture, specialized equipment, some kitchen equipment |

| 15-year property | 15 years | 150% declining balance | Site improvements: driveways, landscaping, fencing, parking, outdoor lighting |

| 27.5-year property | 27.5 years | Straight-line, mid-month convention | Residential rental buildings (the structure itself) |

| 39-year property | 39 years | Straight-line, mid-month convention | Non-residential / commercial buildings (office, retail, industrial) |

The key insight is that MACRS doesn’t say “the whole building is 27.5 years.” MACRS says “assign each asset to the right class.” When you buy a rental property, you’re technically buying hundreds of assets bundled together: the structure itself, but also the appliances inside it, the carpet on the floors, the driveway out front, the landscaping around it. Default treatment lumps all of that into the building and depreciates it over 27.5 years. Proper MACRS treatment separates the components and depreciates each one under its correct class.

How Cost Segregation Reclassifies Components

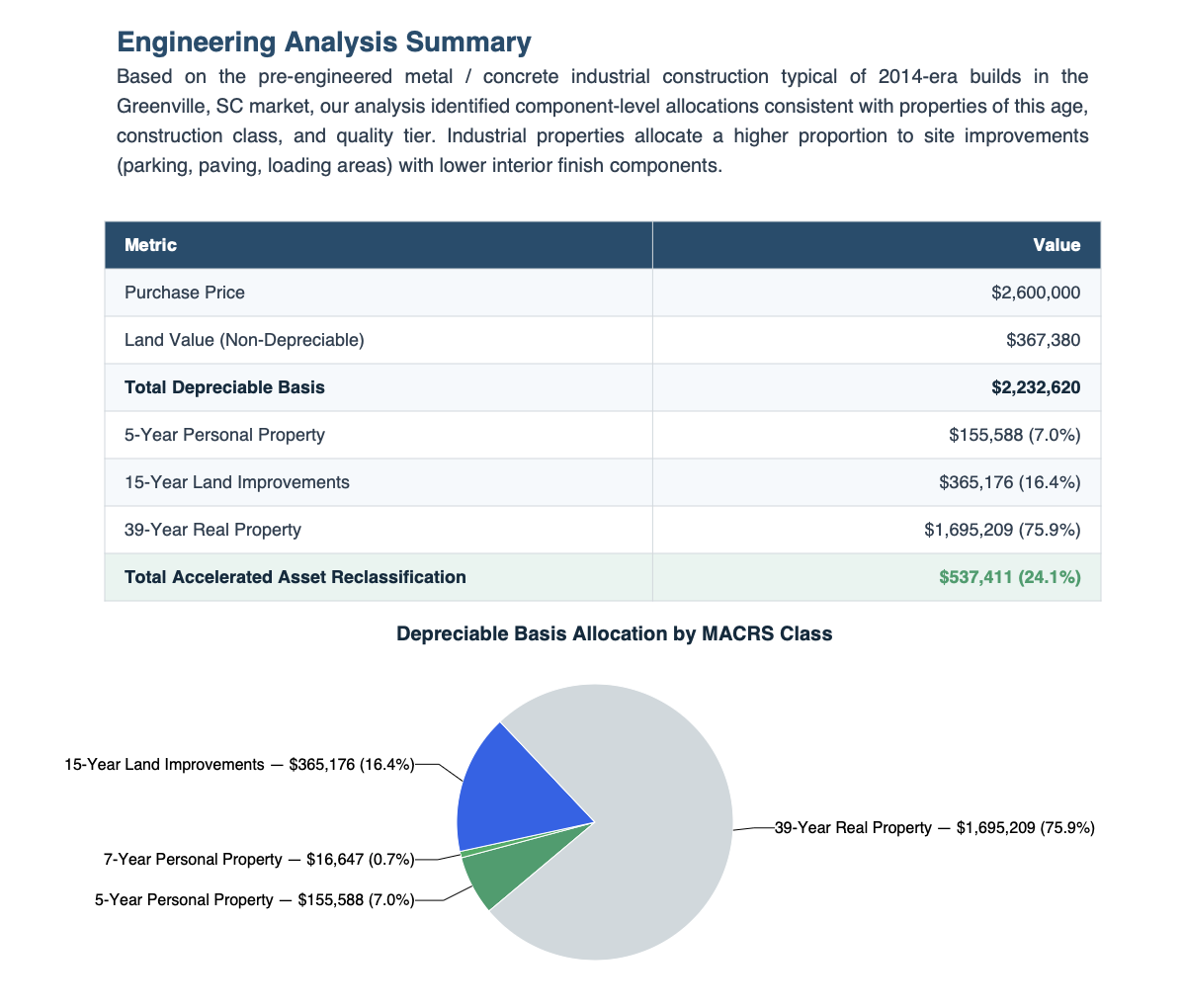

This is where cost segregation lives. It’s the engineering-based process of going through a property and identifying every component that properly belongs in a shorter MACRS class than the building shell. For a typical residential rental, roughly 20-30% of the building basis can be reclassified. For a furnished short-term rental, that number is often 30-40% because of the FF&E (furniture, fixtures, and equipment). For commercial properties with extensive site improvements or specialized interior build-outs, it can go higher. See our breakdown of reclassification percentages by property type for typical ranges.

A qualified cost segregation study does this through a combination of construction cost data (such as national construction cost databases), IRS guidelines, engineering analysis, and component-level allocation. The output is a report that assigns specific dollar amounts to specific MACRS classes, along with documentation that makes the reclassification defensible if the IRS ever asks.

Half-Year vs Mid-Month Conventions

MACRS doesn’t assume you placed an asset in service on January 1. It uses conventions to standardize the partial-year math. There are three, and they matter more than most people realize:

Half-year convention. Most personal property (5, 7, and 15 year classes) uses this. It assumes the property was placed in service at the midpoint of the year, giving you half of the first year’s depreciation regardless of when you actually bought it.

Mid-month convention. Real property (27.5 and 39 year classes) uses this. It assumes the property was placed in service at the middle of the month you actually bought it. Buy in March, you get 9.5 months of depreciation the first year. Buy in November, you get 1.5 months.

Mid-quarter convention. This kicks in if more than 40% of your MACRS personal property (by basis) is placed in service in the fourth quarter. It spreads Q4 depreciation across the quarter. For most individual investors this never comes up. For CPAs managing multiple property placements in December, it’s worth checking.

Bonus Depreciation and How It Stacks with MACRS

Bonus depreciation is a separate first-year deduction under IRC §168(k) that applies to MACRS property with a recovery period of 20 years or less. (For how it compares to the other accelerated option, see Section 179 vs bonus depreciation.) That’s exactly the 5, 7, and 15 year classes that cost segregation reclassifies components into — not the building itself.

Bonus depreciation has moved around a lot. It was 100% from 2017 through 2022, then phased down: 80% in 2023, 60% in 2024, 40% in 2025. But the One Big Beautiful Bill Act signed in July 2025 permanently restored 100% bonus depreciation for property placed in service in 2025 and later. That’s the current state of the law.

When you combine cost segregation with 100% bonus depreciation, the math changes completely. Instead of depreciating reclassified components over 5, 7, or 15 years, you can deduct them all in Year 1.

$500K unfurnished rental — straight-line MACRS vs cost seg with 100% bonus

| Line item | Amount |

| Purchase price | $500,000 |

| Land allocation (20%) | ($100,000) |

| Depreciable basis | $400,000 |

| Standard MACRS Year 1 (27.5 yr straight-line) | $13,818 |

| With cost seg: 25% reclassified to 5/15 year | $100,000 |

| Remaining 27.5 year basis | $300,000 |

| 100% bonus on reclassified + standard on shell | $113,636 |

| Year 1 difference (cost seg vs standard) | $99,818 |

That’s a real example. Same property, same basis, same MACRS rules — just with proper component classification and 100% bonus depreciation applied. At a 37% marginal federal tax rate, that difference is worth about $37,000 in Year 1 tax savings. The study cost $895.

When MACRS Reclassification Makes Sense

Standard MACRS without cost segregation is fine for some situations. For properties under $300K, a $495 study typically still produces positive ROI, but the absolute dollar savings are smaller. For owners in low tax brackets, the same deductions are worth less. And for short holding periods without a 1031 exchange, depreciation recapture on sale can claw back some of the benefit.

Where cost segregation consistently wins is on properties $400K and up, with owners in the 24% bracket or higher, who plan to hold for five or more years. That’s the sweet spot where the engineering-based reclassification into shorter MACRS classes produces genuine, permanent-feeling tax savings. For pricing across cost seg providers, see costsegregationreviews.com — a comparison resource we maintain.

Related Reading

- Cost Segregation vs Standard Depreciation: The Math Side by Side

- What Gets Reclassified? The Cost Segregation Components List

- Is Bonus Depreciation Permanent? What the OBBBA Changed

Frequently Asked Questions What’s the difference between MACRS and straight-line depreciation?

MACRS (Modified Accelerated Cost Recovery System) is the actual depreciation method the IRS requires for most property placed in service after 1986. “Straight-line” is a simpler accounting concept — it spreads depreciation evenly over the recovery period. MACRS for real property (27.5 or 39 years) uses the straight-line method with a half-year or mid-month convention. MACRS for shorter-life property (5, 7, 15 years) uses double-declining balance, which front-loads the depreciation. Cost segregation is about reclassifying components into those shorter MACRS classes. Can I change MACRS methods mid-way through ownership?

Yes — a cost segregation study is essentially a mid-ownership method change. You use Form 3115 to file the accounting method change and a Section 481(a) adjustment to catch up the depreciation you should have taken under the new method. The IRS has permitted this for decades and it’s a routine filing when supported by an engineering-based study. Does MACRS change if I sell the property?

MACRS doesn’t change, but depreciation recapture rules apply. When you sell, you have to “pay back” a portion of the depreciation at up to 25% under IRC §1250 for real property and at ordinary rates under IRC §1245 for shorter-life personal property like appliances and furnishings. Cost segregation creates more §1245 property, which means more potential recapture — but the time value of the accelerated deductions usually still wins, especially if you hold the property for 5+ years or use a 1031 exchange. What’s the mid-quarter convention and does it apply to me?

The mid-quarter convention kicks in if more than 40% of your MACRS depreciable property (by basis) is placed in service in the last three months of the tax year. It spreads that fourth-quarter depreciation across the quarter it was placed in service rather than assuming a mid-year convention. For most individual investors this doesn’t come up. For CPAs managing multiple property placements in Q4, it’s worth checking. Is bonus depreciation separate from MACRS?

Bonus depreciation is an additional first-year deduction on top of regular MACRS. It applies to property with a MACRS recovery period of 20 years or less — which is exactly the 5, 7, and 15 year classes that cost segregation reclassifies components into. For property placed in service in 2025 and later, the One Big Beautiful Bill Act restored bonus depreciation to 100%, meaning the entire reclassified basis can be deducted in Year 1. See our breakdown of what the OBBBA changed. Why do rentals use 27.5 years instead of 39?

MACRS sets 27.5 years for “residential rental property” (where 80%+ of gross rental income is from dwelling units) and 39 years for non-residential commercial buildings. Short-term rentals and Airbnbs that meet the residential definition still use 27.5 years even if they have commercial-style operations. Mixed-use properties split between the two based on the square footage or rental income allocation.

See What MACRS Reclassification Is Worth on Your Property

Free preliminary depreciation estimate — property summary, basis allocation, five-year schedule. We do the work; you get the PDF.

See my estimated Year-1 savings →Frequently asked

What's the difference between MACRS and straight-line depreciation?

MACRS (Modified Accelerated Cost Recovery System) is the actual depreciation method the IRS requires for most property placed in service after 1986. Straight-line is a simpler accounting concept — it spreads depreciation evenly over the recovery period. MACRS for real property (27.5 or 39 years) uses the straight-line method with a half-year or mid-month convention. MACRS for shorter-life property (5, 7, 15 years) uses double-declining balance, which front-loads the depreciation. Cost segregation is about reclassifying components into those shorter MACRS classes.

Can I change MACRS methods mid-way through ownership?

Yes — a cost segregation study is essentially a mid-ownership method change. You use Form 3115 to file the accounting method change and a Section 481(a) adjustment to catch up the depreciation you should have taken under the new method. The IRS has permitted this for decades and it's a routine filing when supported by an engineering-based study.

Does MACRS change if I sell the property?

MACRS doesn't change, but depreciation recapture rules apply. When you sell, you have to pay back a portion of the depreciation at up to 25% under IRC §1250 for real property and at ordinary rates under IRC §1245 for shorter-life personal property like appliances and furnishings. Cost segregation creates more §1245 property, which means more potential recapture — but the time value of the accelerated deductions usually still wins, especially if you hold the property for 5+ years or use a 1031 exchange.

What's the mid-quarter convention and does it apply to me?

The mid-quarter convention kicks in if more than 40% of your MACRS depreciable property (by basis) is placed in service in the last three months of the tax year. It spreads that fourth-quarter depreciation across the quarter it was placed in service rather than assuming a mid-year convention. For most individual investors this doesn't come up. For CPAs managing multiple property placements in Q4, it's worth checking.

Is bonus depreciation separate from MACRS?

Bonus depreciation is an additional first-year deduction on top of regular MACRS. It applies to property with a MACRS recovery period of 20 years or less — which is exactly the 5, 7, and 15 year classes that cost segregation reclassifies components into. For property placed in service in 2025 and later, the One Big Beautiful Bill Act restored bonus depreciation to 100%, meaning the entire reclassified basis can be deducted in Year 1.

Why do rentals use 27.5 years instead of 39?

MACRS sets 27.5 years for residential rental property (where 80%+ of gross rental income is from dwelling units) and 39 years for non-residential commercial buildings. Short-term rentals and Airbnbs that meet the residential definition still use 27.5 years even if they have commercial-style operations. Mixed-use properties split between the two based on the square footage or rental income allocation.